Oracle beats and the CPI surprise: what Wednesday gave tech investors

May CPI came in at 4.0% YoY — below the 4.2% consensus — softening but not erasing rate-hike fears ahead of June 17 FOMC. Oracle posted better-than-expected Q4 FY2026 earnings and projected strong cloud growth, though after-hours trading turned cautious. SpaceX's roadshow closed at 4x oversubscribed ($250B demand vs. $75B raise); pricing is Thursday, first trade Friday. Adobe reports Thursday with a split analyst camp: Stifel raised to $400 Buy, TD Cowen cut to $285 Hold.

リサーチノート

Wednesday handed tech investors two immediate reads — a cooler-than-feared inflation print before the open and Oracle's fiscal fourth-quarter earnings after the close — against the continued overhang of a 4x-oversubscribed SpaceX roadshow and Adobe's earnings tomorrow night.

The May CPI print: below the 4.2% consensus

Consumer prices rose 4.0% year-over-year in May, a meaningful step down from April's 4.9% and below the 4.2% Wall Street expected.12 Core CPI — stripping out food and energy — was estimated at 2.9% YoY coming in, reflecting Iran-war driven energy price pressure fading at the headline level while services stayed sticky.3

The print matters because rate-hike expectations are still live. After last Friday's blowout 172K payroll report, traders had pushed year-end hike odds toward 70%. A softer CPI reading complicates the case for a first move in June 17's FOMC meeting — but does not close it, given core stickiness. The dot plot remains the wildcard: Fed Chair Kevin Warsh has signaled he could eliminate the dot plot entirely, which would strip the market's clearest signaling channel right before a potentially pivotal meeting.4

A Reuters poll found 70 of 102 economists expected rates to stay in the current 3.50%–3.75% range through year-end — a view that becomes harder to hold if May core inflation remains elevated and payrolls don't cool quickly.14

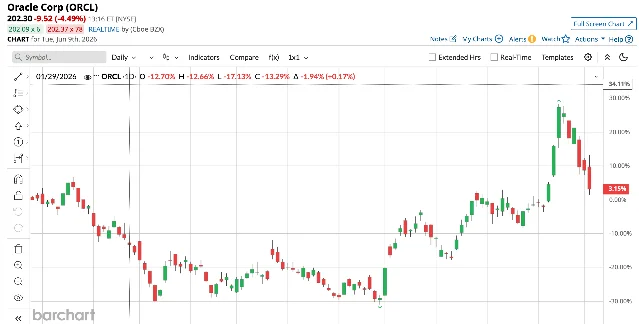

Oracle Q4 FY2026: better than feared

Oracle reported better-than-expected earnings and revenue for fiscal Q4 2026 and projected strong growth in its cloud business.5 Consensus had the quarter at $1.96 non-GAAP EPS and ~$19.1B revenue (roughly +20% YoY), alongside official guidance issued in Q3 of $1.92–$1.96 EPS and 18–20% revenue growth.6

The numbers everyone was watching most closely:

| Metric | Q3 FY2026 (prior quarter) | Q4 consensus expectation |

|---|---|---|

| Total cloud revenue | ~$8.9B (+43.5% YoY) | — |

| OCI (Oracle Cloud Infrastructure) | +84% YoY | Need ≥28% to hold story |

| RPO (backlog) | $553B (+325% YoY) | Conversion to billed revenue |

| Non-GAAP EPS | $1.79 (beat) | $1.96 |

| Total revenue | $17.19B (+21.7%) | ~$19.1B |

The AI infrastructure narrative at Oracle hinges less on whether EPS beats and more on whether RPO is converting: the company's remaining performance obligations surged 325% to $553B last quarter, driven by multi-year AI data center contracts.6 BNP Paribas analyst Stefan Slowinski was watching for capex guidance in the range of $80–100B for FY2027 — funds earmarked for Stargate campus expansion and Nvidia GPU purchases.6

Wall Street went into the print fairly constructive: 33 of 43 covering analysts held Strong Buy, average target price $254, with Evercore ISI raising its target to $245 (from $220) and Oppenheimer lifting to $275 (from $235) in the run-up.6 The options market had priced in a 4–5% move, and MarketWatch's intraday competitor data showed ORCL down roughly 5.75% in after-hours, suggesting either guidance came in softer than the "strong growth" headline or near-record AI capex expectations weighed on the read-through.

The stock entered earnings having already sold off nearly 9.6% on June 5 — caught in the same Broadcom-sparked AI infrastructure credibility reset that swept the Philadelphia Semiconductor Index down more than 8% intraday that session.7

SpaceX: $250B of demand for a $75B raise

The roadshow wraps Thursday. SpaceX has drawn more than $250 billion in investor demand for an offering that seeks to raise $75B — roughly 3.5–4x oversubscribed, and still growing as long-term fund orders remain open.8 The share price is fixed at $135, implying a valuation of approximately $1.75–1.8 trillion — about 100x 2025 sales of $18.7B.9 The ticker SPCX is expected to begin trading on Nasdaq Friday, June 12.

The roadshow pitch centers on three layers: the core launch business (which captured most of orbital payload capacity for the past three years), Starlink's rapidly scaling subscription revenue, and an AI infrastructure angle — SpaceX argues it is the only company positioned to deploy data center capacity into orbit, relevant as U.S. terrestrial power constraints tighten.8

For the broader tech market, the SpaceX listing adds a second overhang beyond macro. At $75B in new shares hitting the float on Friday, the IPO creates real rotation pressure — money that moves into SPCX has to come from somewhere, and near-term growth names with stretched valuations are the obvious source.

Adobe tomorrow: down 30% YTD, watching for a floor

Adobe reports Q2 FY2026 after the close Thursday, June 12. Analysts expect $5.95 non-GAAP EPS and $6.59B revenue from the consensus.10 The stock is down roughly 30% year-to-date, and two diverging analyst views frame the setup:

- Stifel maintained its Buy rating and raised its price target to $400 (from $350), expecting roughly 1.5% organic revenue growth and flagging AI integration as a longer-term positive.11

- TD Cowen kept its Hold rating and cut its price target to $285, citing slowing growth trends ahead of the quarter.12

The central tension: Adobe's Firefly AI tools are generating revenue, but the pace of creative subscription growth has slowed enough to raise questions about whether Firefly expands the addressable market or cannibalizes users who previously needed the full Creative Cloud stack. Any upside surprise on annual recurring revenue (ARR) or a raise in full-year guidance would be the signal bulls need. A guidance cut would likely push ADBE toward its year-to-date lows.

What to watch Thursday and Friday

| Event | Timing | What matters |

|---|---|---|

| Adobe Q2 FY2026 earnings | Thu June 12, after close | ARR growth, full-year guidance, Firefly monetization commentary |

| SpaceX pricing confirmed | Thu June 12 | Final allocation; any upsizing of the offering size |

| SPCX first day of trading | Fri June 13 | IPO pop, post-open stabilization, sector rotation read-through |

| FOMC blackout period | Active through June 17 | No Fed commentary; rate futures move on CPI/data only |

The June 17 FOMC meeting is now the gravitational center. A CPI print below consensus today removed the most hawkish marginal scenario, but the core rate is sticky enough that a Warsh-led Fed could still surprise. The Nasdaq's current level — around 25,900 after Tuesday's -1% close — remains hostage to that outcome.13

参考ソース

- 1Kiplinger — What to Expect From the May CPI Report

- 2Yahoo Finance — CPI: US inflation likely continued to heat up last month

- 3Investopedia — What To Expect From Wednesday's Report On Inflation

- 4Saxo Bank — Market Quick Take — 9 June 2026

- 5Schwab Network via Facebook

- 6Barchart — Oracle Stock Is Careening Toward Earnings with a Heavy $100 Billion Weight on Its Back

- 7TheStreet via AOL

- 8Reuters — SpaceX IPO demand is approaching four times oversubscribed

- 9Barron's — A SpaceX Stock IPO Pop? How Much Will It Jump

- 10ChartMill — Adobe analyst ratings

- 11GuruFocus — Adobe Falls 23% YTD As Analysts Raise Questions Ahead Of Earnings

- 12TIKR — TD Cowen Slashes Adobe Stock Target Price

- 13Reuters — S&P 500, Nasdaq fall as tech selling resumes

- 145ref|Reuters — Fed to hold rates this year, cut calls fade|https://www.reuters.com/business/fed-hold-rates-this-year-cut-calls-fade-war-inflation-persists-economists-say-2026-06-09/

このコンテンツについて、さらに観点や背景を補足しましょう。